We have prepared some commentary around the Federal Budget which was released a month earlier than usual last night, ahead of the much anticipated 2019 Federal Election.

We have prepared some commentary around the Federal Budget which was released a month earlier than usual last night, ahead of the much anticipated 2019 Federal Election.This pre election Federal Budget and the Opposition Budget reply later in the week, will all form part of the election campaign (which based on some adverts already feels a little to long in my view).

This is the first Federal Budget of new Treasurer Josh Frydenberg who has been able to announce the first budget surplus in over 11 years. Keep in mind that the surplus Budget is an expectation only and just like our personal cash flow requires accountability and discipline to succeed. The expected $7.1 Billion surplus (on the income and expense side of things) is a long way from the current debt levels the Australian Government is carrying (the assets and liabilities side of the equation).

We have prepared a summary of the key measures for Individuals, Superannuation, Social Security and for Companies below:

- Increase to Low and Middle Income Tax Offset (for income earners between $48,000 – $90,000) to start for the current income year 2019 through to 2022;

From 1 July 2018 to 30 June 2022:

Increase the Low and Middle Income Tax Offset (LMITO) from a maximum of $530 to $1,080 ($2,160 for dual income families). The LMITO (which is in addition to the Low Income Tax Offset) will be received after individuals lodge their tax return for the relevant income years.

From 1 July 2022:

The upper threshold for the 19% tax bracket will increase from $41,000 to $45,000, and the LMITO maximum amount will increase from $645 to $700. The increased LMITO will be withdrawn at a rate of 5 cents per dollar between taxable incomes of $37,500 and $45,000. LITO will then be withdrawn at a rate of 1.5 cents per dollar between taxable incomes of $45,000 and $66,667.

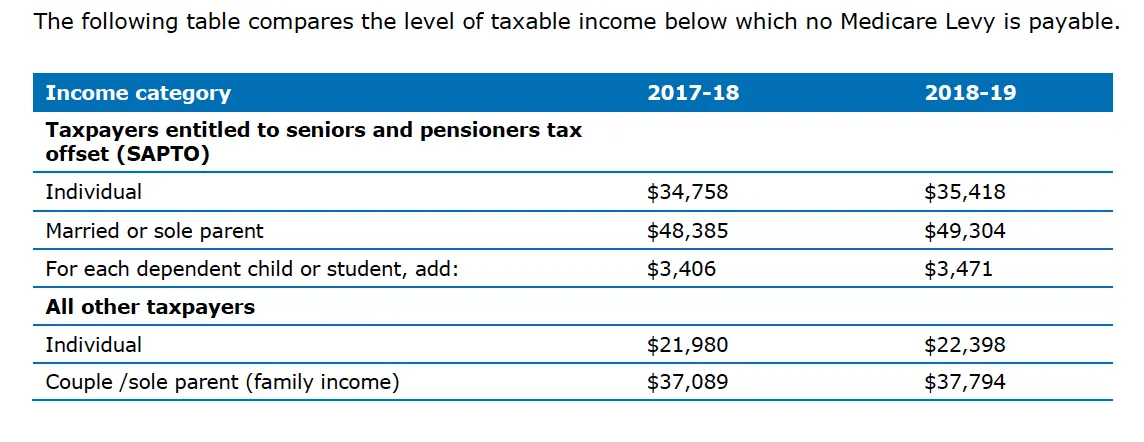

- Increase to Medicare Levy threshold for Singles and Families;

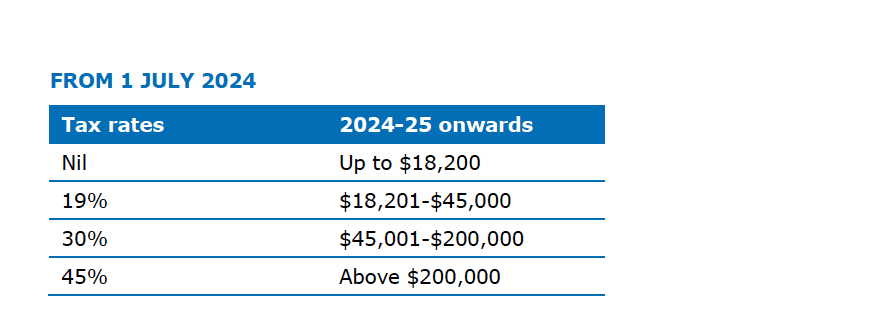

- From 2024 proposed changes to marginal tax rates to reduce the 32.5 percent tax rate down to 30 percent and removal of the 37 percent tax rate so all income earners under $200,000 would pay no more than 30 cents in the dollar;

- Super Contribution allowances to align to age pension age of 67. People up to age 67 can make contributions to super accounts without meeting the work test;

- Non-concessional contribution cap bring forward rules to adjust to age 67 rule above;

- Spouse contributions acceptance to be increased from age 69 to age 74;

From July 1 2020, Australians aged 65 and 66 will now be able to make voluntary superannuation contributions, both concessional and non-concessional, without meeting the Work Test. Previously, this was only available to individuals below 65.

This will align the Work Test with the eligibility age for the Age Pension, which is scheduled to reach 67 from 1 July 2023. There are around 55,000 Australians aged 65 and 66 who will benefit from this reform in 2020-21.

This also includes extending access to the bring-forward arrangements to individuals aged 65 and 66 which allows individuals to make three years’ worth of non-concessional contributions to their super in a single year.

The Government has also increased the age limit for spouse contributions from 69 to 74. Currently, those aged 70 years and over cannot receive contributions made by another person on their behalf.

The Work-Test-Exemption which allows individuals a further year to voluntarily contribute to superannuation after they have finished working will still apply to individuals from 67 to 74.

- Self Managed Super Fund income stream tax calculations to be streamlined for those with both accumulation and pension interests.

The Government will streamline administrative requirements for the calculation of exempt current pension income (ECPI).

The Government will allow superannuation fund trustees with interests in both the accumulation and retirement phases during an income year to choose their preferred method of calculating ECPI. This change will reduce unnecessary red-tape for SMSFs in pension phase.

- One off Energy Assistance Payment for 2018-19 income year of $75 for singles and $125 for couples on social security payments;

Social security pension recipients will receive a one-off Energy Assistance Payment by the end of the current financial year. The payment will be $75 for singles and $125 for couples combined and will be exempt from income tax.

People who are Australian residents and eligible for the following payments as at 2 April 2019 will automatically receive the payment – Age Pension, Disability Support Pension, Carer Payment and Parenting Payment Single. Also recipients of the following payments from the Department of Veterans Affairs will be eligible – Service Pension, Income Support Supplement, disability payments, War Widow(er)s Pension, and permanent impairment payments under the Military Rehabilitation and Compensation Act 2004 (including dependent partners) and the Safety, Rehabilitation and Compensation Act 1988.

- Allocation of funds for one off increase to Aged Care Basic Subsidy and further funding for home care packages.

The Government will provide $724.8 million over five years from 2018-19 to fund improvements in residential and home care services, including:

- a one-off increase to the basic subsidy for residential aged care recipients from 2018-19 and 13,500 additional residential aged care places

- 10,000 additional home care packages from 2018-19. Home care packages to be provided across the four package levels

- an increase to the dementia and the veterans’ home care supplements

- funding to strengthen aged care regulation.

- Extending the Immediate Deductible Threshold for asset write off purchase will increase from $25,000 to $30,000 from Budget Night (2 April 2019) until 30 June 2020. Entity turnover levels to access this will increased from $10M to $50M;

The Government is proposing to increase and expand access to the instant asset write-off from Budget night until 30 June 2020. These changes are in addition to a measure announced on 29 January 2019 that is currently before Parliament and is yet to be legislated.

The Government announced two changes in the Budget:

- increasing the instant asset write-off threshold from the proposed $25,000 to $30,000 for small businesses (with aggregated annual turnover of less than $10 million)

- expanding the instant asset write-off measure to medium sized businesses with aggregated annual turnover of $10 million or more, but less than $50 million.

This means both small businesses and medium sized businesses can immediately deduct purchases of eligible assets costing less than $30,000 that are first used, or installed ready for use, from Budget night to 30 June 2020. Medium sized businesses must also acquire these assets after Budget night to be eligible as they have previously not had access to the instant asset write-off. The $30,000 threshold applies on a per asset basis. This means eligible businesses can instantly write off multiple assets.

As always if you have any questions with regards to your current arrangements please do not hesitate in contacting me at the office 1300 772 643 and remember based on the election cycle many of these proposed measures may not eventuate.

Scott Malcolm has been awarded the internationally recognised Certified Financial Planner designation from the Financial Planning Association of Australia and is Director of Money Mechanics. Money Mechanics is a fee for service financial advice firm who partner with clients in Melbourne, Canberra, Newcastle and Sydney to achieve their life and wealth outcomes. Money Mechanics Pty Ltd (ABN 64 136 066 272) is a Corporate Authorised Representative (No. 336429) of Infocus Securities Australia Pty Ltd (ABN 47 097 797 049) AFSL and Australian Credit Licence No. 236523

The information provided on this article is of a general nature only. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information you should consider its appropriateness having regard to your own objectives, financial situation and needs.