As a pre-election year Budget this year there are some tax benefits being provided as well as some small tweaks to the tax, super and social security system

As a pre-election year Budget this year there are some tax benefits being provided as well as some small tweaks to the tax, super and social security system

We have provided some of the highlights to Budget 2018, so grab your morning coffee or tea and if you have any questions please do not hesitate in contacting us at the office.

Before reading the below note that these are only announcements and will require passage through Parliament before being legislated.

From 1 July 2019, the Medicare levy was proposed to be increased to 2.5% to help fund the National Disability Insurance Scheme. Based on better than expected revenue at the mid year budget review this increase has been removed and the Medicare Levy will remain at 2%.

There are some personal tax cuts however the bulk of these do not come into effect until 2024 which is a long time-frame for anyone in politics!

Property Investors saw some changes last budget with the last year and this year the Government announced that they would no longer allow tax deductions on vacant land.

In the superannuation space the already announced increase to Self Managed Super Fund members was ‘reaffirmed’ with the number of members in a Self Managed Fund increasing from 4 – 6 members. For SMSF’s with good compliance history a 3 year audit approach has been announced which may reduce fees for some SMSF.

For people under age 25 there has been an announcement on an ‘opt in’ provision for insurance cover as well as announcements across the board for maximum fees which can be charged in some super accounts – which on the back of the Royal Commission into the sector is good news for consumers who are not actively engaged in their super strategies.

For people over 65 with less than $300,000 in super there is an announcement to remove the work test requirement to move funds into superannuation.

In the aged care space there have been announcements to help people stay in their homes longer with in house care and support options.

See the further details below.

Financial Service and Education

Modernising Payroll and Super Fund Reporting

The Government will provide an additional $15.0 million over three years from 2018-19 to the Australian Taxation Office to support the modernisation of payroll and superannuation fund reporting. The funding will be used to support small businesses with fewer than 20 employees during the transition to Single Touch Payroll Reporting from 1 July 2019.

Funding for this measure has already been provided for by the Government. This measure builds on the 2017-18 Mid Year Budget measure titled Superannuation Guarantee Integrity Package — modernising payroll and superannuation fund reporting.

Australian Securities and Investments Commission – improving financial literacy for Women

The Government will provide $10.0 million to the Australian Securities and Investments Commission in 2018-19 to provide a grant that will support initiatives to enhance female financial capability. For some great resources checkout http://www.moneysmart.gov.au

Royal Commission into Misconduct in the Banking, Financial Services and Superannuation Industry

The Government will provide $10.6 million over two years from 2017-18 to the Australian Securities and Investments Commission (ASIC) and $2.7 million in 2018-19 to the Australian Prudential Regulation Authority (APRA) to assist in their involvement in the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. The cost of this measure will be offset by an increase in the APRA Financial Institutions Supervisory Levies of $2.7 million in 2018-19 and an increase in levies of $10.6 million over two years from 2018-19 under the ASIC industry funding model.

Funding of $5.9 million for ASIC in 2017-18 has already been provided for by the Government.

Personal taxation

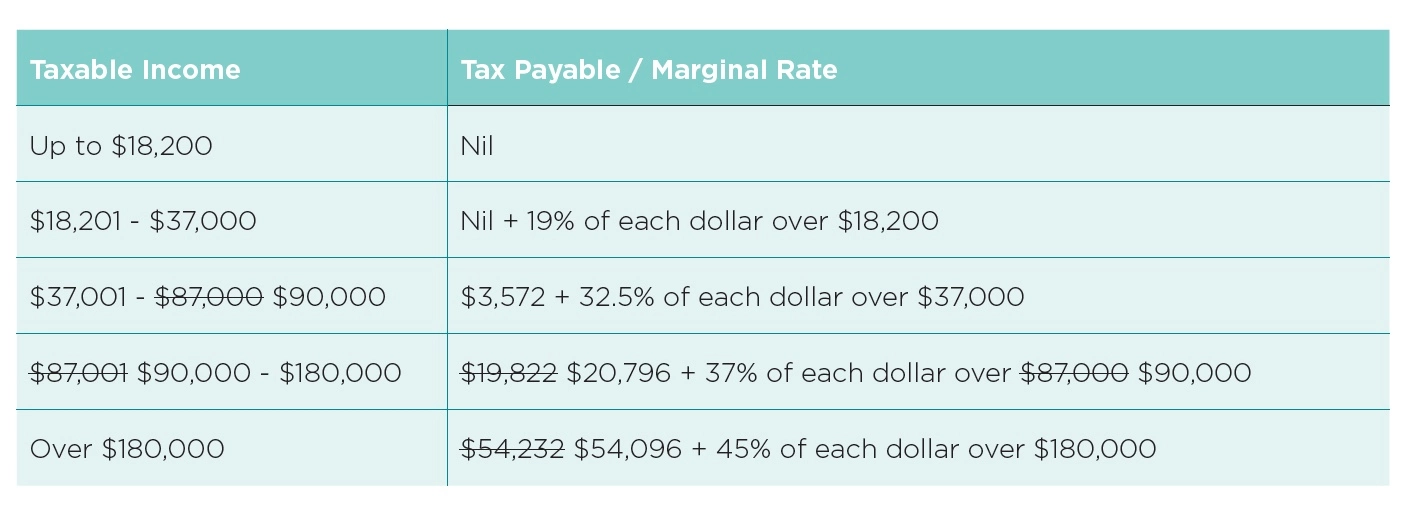

Personal Income Tax – The tax rates for 2018-19

The top threshold of 32.5 per cent personal income tax bracket will be increased from $87,000 to $90,000. This measure takes effect from 1 July 2018.

Personal Income Tax — retaining the Medicare levy rate at 2 per cent

The Medicare levy rate will no longer be increased from 2.0 to 2.5 per cent of taxable income from 1 July 2019.

Medicare Levy low-income threshold for families

The Government will increase the Medicare Levy low-income threshold for singles, families and single seniors and pensioners from 2017-18 income year.

• The threshold for singles will be increased from $21,655 to $21,980.

• The family threshold will be increased from $36,541 to $37,089.

• For single seniors and pensioners, the threshold will be increased from $34,244 to $34,758.

• The family threshold for seniors and pensioners will be increased from $47,670 to $48,385.

• For each dependent child or student, the family income thresholds increase by a further $3,406, instead of the previous amount of $3,356.

Personal Income Tax — income tax exemption for certain Veteran Payments

Veteran Payments and supplementary amounts (such as pension supplement, rent assistance and remote area allowance) of Veteran Payment paid to a veteran, and full payments (including the supplementary component) made to the spouse or partner of a veteran who dies, are exempt from income tax are exempt from income tax. This measure takes effect from 1 May 2018.

Personal Income Tax Plan

The Government will introduce a seven-year Personal Income Tax Plan over three stages resulting in the removal of the 37% marginal tax rate by 1 July 2024.

- top threshold of 32.5 per cent personal income tax bracket will be increased from $120,000 to $200,000.

- Taxpayers will pay the top marginal tax rate of 45 per cent from taxable incomes exceeding $200,000 and the 32.5 per cent tax bracket will apply to taxable incomes of $41,001 to $200,000.

Taxation of income based on fame and image

From 1 July 2019, income generated based on a person’s fame or image will no longer be able to be assigned to other entities through licencing agreements and will be included in the individual’s assessable income. This is to remove the ability for individuals to assign licencing rights to related party companies and trusts to have income generated based on their personal fame or image taxed at a lower rate than their marginal rate.

Wealth Creation – Tax Strategies and Trusts

Enhancing the integrity of concessions in relation to partnerships

Partners that alienate their income by creating, assigning or otherwise dealing in rights to the future income of a partnership will no longer be able to access the small business capital gains tax (CGT) concessions in relation to these rights.

This measure will take effect from 7:30PM (AEST) on 8 May 2018.

Extending anti-avoidance rules for circular trust distributions

Anti-avoidance measures will be extended to family trusts engaging in ‘round robin’ arrangements whereby the trusts act as beneficiaries of each other and the distribution is ultimately returned to the original trustee tax free.

This measure will apply from 1 July 2019.

Improving the taxation of testamentary trusts

Concessional tax rates for minors receiving income from testamentary trusts will be limited to income derived from assets that are transferred from the deceased estate or the proceeds of the disposal or investment of those assets. This is to prevent taxpayers from inappropriately obtaining the concession in respect of income on assets unrelated to the deceased estate into the testamentary trust.

This measure will apply from 1 July 2019.

MM Comment – this will be unlikely to impact the majority of Testamentary Trusts based on how they are setup and where the asset comes from.

Removing the capital gains discount at the trust level for Managed Investment Trusts

Managed Investment Trusts will no longer be able to apply the 50 per cent capital gains discount at the trust level. This measure will prevent beneficiaries that are not entitled to the Capital Gains Tax (CGT) discount in their own right from getting a benefit from the CGT discount being applied at the trust level. The measure will not stop the CGT discount applying in the hands of beneficiaries of a distribution from the trust.

This measure will apply from 1 July 2019.

Deny deductions for vacant land

Expenses associated with holding vacant land will no longer be tax deductible. This measure is to ensure no deductions are claimed for vacant land that is not genuinely held for the purpose of earning assessable income.

This measure will take effect from 1 July 2019.

Company Tax – Improving the integrity of the tax treatment of concessional loans between tax exempt entities

Where tax exempt entities become taxable after 8 May 2018, the Government will disallow tax deductions that arise on the repayment of the principal of a concessional loan.

Under this measure, concessional loans that are entered into by tax exempt entities that become taxable will be required to be valued as if they were originally entered into on commercial terms.

Small business – Further extending the immediate deductibility threshold

The $20,000 instant asset write-off will be extended by a further 12 months to 30 June 2019 for businesses with aggregated annual turnover less than $10 million.

Small businesses will be able to immediately deduct purchases of eligible assets costing less than $20,000 first used or installed ready for use by 30 June 2019. Only a few assets are not eligible (such as horticultural plants and in-house software).

Assets valued at $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool and depreciated at 15 per cent in the first income year and 30 per cent each income year thereafter. This asset pool can also be immediately deducted if the balance is less than $20,000 over this period.

Superannuation

Capping passive fees, banning exit fees and reuniting small and inactive superannuation accounts

There will be a three per cent annual cap on passive fees charged by superannuation funds on accounts with balances below $6,000, and exit fees will be banned on all superannuation accounts.

In addition, all inactive superannuation accounts with balances below $6,000 will need to be transferred to the ATO. These changes will take effect from 1 July 2019.

If you havent already done a Super Search check out the awesome super consolidation tools online at www.my.gov.au

Changes to insurance in superannuation

Insurance in superannuation will only be able to be offered on an opt-in basis for:

• members with low balances of less than $6,000;

• members under the age of 25 years; and

• members whose accounts have not received a contribution in 13 months and are inactive.

The changes will take effect on 1 July 2019.

Affected superannuants will have a period of 14 months to decide whether they will opt-in to their existing cover or allow it to switch off.

Better integrity over deductions for personal contributions

Funding will be provided to the ATO to improve the integrity of the ‘notice of intent’ (NOI) processes for claiming personal superannuation contribution tax deductions. Currently, some individuals are claiming the deduction without submitting the Notice of Intent. As a result, no tax is paid on the contribution amount.

This measure will commence from 1 July 2018.

Increasing the maximum number of allowable members in self-managed superannuation funds and small APRA funds from four to six

The maximum number of members permitted in new and existing self-managed superannuation funds and small APRA funds will be increased from four to six.

This measure will commence from 1 July 2019.

Preventing inadvertent concessional cap breaches by certain employees

Individuals whose income exceeds $263,157 and have multiple employers will be able to nominate that their wages from certain employers are not subject to the superannuation guarantee (SG) from 1 July 2018.

The measure will allow eligible individuals to avoid unintentionally breaching the $25,000 annual concessional contributions cap as a result of multiple compulsory SG contributions.

This measure will commence from 1 July 2018.

Three-yearly audit cycle for some self-managed superannuation funds

Self-managed superannuation funds with a history of good record-keeping and compliance will be subject to a three-yearly audit requirement rather than an annual audit requirement.

This measure will start on 1 July 2019.

More Choices for a Longer Life — comprehensive income products in retirement

The superannuation law will be amended to introduce a retirement covenant that will require superannuation trustees to formulate a retirement income strategy for superannuation fund members. The Government will also amend the Corporations Act 2001 to introduce a requirement for providers of retirement income products to report simplified, standardised metrics in product disclosure to assist customer decision making.

More Choices for a Longer Life — work test exemption for recent retirees

The Government will introduce an exemption from the work test for voluntary contributions to superannuation, for people aged 65-74 with superannuation balances below $300,000, in the first year that they do not meet the work test requirements.

This measure will take effect from 1 July 2019.

Social Security and Family Payments

More choices for a longer life – finances for a longer life

• Increase the Pension Work Bonus from $250 to $300 per fortnight to allow pensioners to earn up to $7,800 each year without impacting their pension;

• Extend the Pension Work Bonus to allow self-employed retirees to earn up to $300 per

fortnight without impacting their pension;

• Amend the pension means test rules to encourage the development and take-up of lifetime retirement income products that can help retirees manage the risk of outliving their savings; and

• Expand the Pension Loans Scheme to everyone over Age Pension age and to increase the

maximum fortnightly income stream to 150 per cent of the Age Pension rate.

This measure commences on 1 July 2019.

More Choices for a Longer Life — healthy ageing and high quality care

The Government will implement new policies to support people to stay at home longer, remain healthy and independent for longer, and to improve access to high quality, safe aged care:

• additional 14,000 new high level home care packages over four years from 2018-19 in addition to the 6,000 high level packages delivered in the 2017-18 MYEFO;

• 13,500 residential aged care places and 775 short term restorative care places in the 2018-19 Aged Care Approvals Round will be released, with a $60.0 million capital investment to support new places;

• combine the Residential Care and Home Care programs from 1 July 2018 to provide greater flexibility to respond to changes in demand for home care packages and residential aged care places.

• the Government will support preparatory work for a new national assessment framework for people seeking aged care;

• the Government will to trial navigator services to assist people seeking information about aged care to make decisions that are right for them.

More Choices for a Longer Life — jobs and skills for mature age Australians

To support mature age Australians to adapt to the transitioning economy and develop the skills needed to remain in work, additional funding includes:

- targeted training to help mature age job seekers aged 45 years and over and who are

registered with a jobactive provider to enhance employability, develop digital skills and identify opportunities in local labour markets; - training funding of up to $2,000 for workers aged 45 to 70 years to take up reskilling or upskilling opportunities, with the Government contribution to be matched by either the worker or their current employer;

- support mature age workers who are considering early retirement or who are retrenched to look at alternatives to remain in employment;

- additional Inclusive Entrepreneurship Facilitators for an increased focus on mature age people to promote entrepreneurship and new business opportunities and to provide business mentoring; and

- restructure the Employment Fund to allow additional wage subsidy places for mature age employees. In addition, the Government will work with business and community peak bodies to develop strategies that promote the benefits of a diverse workforce, influence hiring practices and reduce discrimination.

More Choices for a Longer Life — skills checkpoint for older workers program

The Government will establish the Skills Checkpoint for Older Workers program, which will support employees aged 45-70 to remain in the workforce.

From 1 September 2018, 5,000 employees each year would be entitled to receive customised career advice on transitioning into new roles, or their pathways to a new career, including referrals to relevant training options

National Disability Insurance Scheme — continuity of support

The Government will ensure continuity of support for people who are not eligible for the National Disability Insurance Scheme (NDIS), but are currently receiving support under programs that are transitioning to the NDIS.

Under the new continuity of support arrangements, eligible recipients will receive a level of support that is consistent with that which they currently receive.

Delivering Australia’s Digital Future — Welfare Payment Infrastructure Transformation — Tranche Three

Tranche Three will transform the delivery of payments to jobseekers, older Australians, carers and people with disabilities by implementing more efficient and automated claim, assessment and payment processes.

Implications for Australian assets

Commentary from Dr Shane Oliver – AMP Capital Investors.

Cash and term deposits – with interest rates remaining low, returns from cash and bank term deposits will remain low.

Bonds – a major impact on the bond market from the Budget is unlikely. With Australian five year bond yields at 2.4%, it’s hard to see great returns from bonds over the next few years albeit Australian bonds will likely outperform US/global bonds.

Shares – the potential boost to confidence from this Budget could be a small positive for the Australian share market. But it’s hard to see much impact on shares.

Property – the Budget is unlikely to have much impact on the property market. Interesting to note that the 2017 budget saw an effort to encourage retirees to sell the family home whereas this year there are measures to help them stay in it! We expect Sydney and Melbourne home prices to fall further.

Infrastructure – continuing strong infrastructure spending should in time provide more opportunities for private investors as many of the resultant assets are ultimately privatised.

The $A – the Budget alone won’t have much impact on the $A. With the interest rate differential in favour of Australia continuing to narrow the downtrend in the $A has further to go.

Scott Malcolm has been awarded the internationally recognised Certified Financial Planner designation from the Financial Planning Association of Australia and is Director of Money Mechanics. Money Mechanics is a fee for service financial advice firm who partner with clients in Melbourne, Canberra and Sydney to achieve their life and wealth outcomes. We are authorised to provide financial advice through PATRON Financial Advice AFSL 307379.

The information provided on this article is of a general nature only. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information you should consider its appropriateness having regard to your own objectives, financial situation and needs.